1.10.3

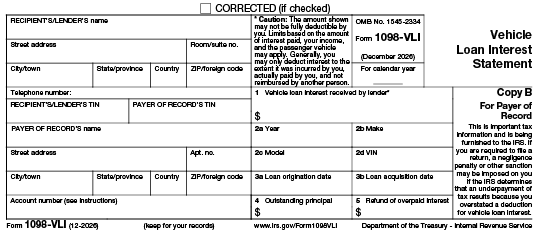

Section 70203 of the One Big Beautiful Bill Act creates a brand-new above-the-line deduction of up to $10,000 per year for interest paid on a qualified passenger-vehicle loan. The deduction is available to itemizers and non-itemizers alike for tax years 2025 through 2028 (it sunsets after 12/31/2028 unless extended). Eligibility is narrower than the headline suggests: the vehicle must be new, for personal use, and have its final assembly in the U.S.; the loan must be incurred after 12/31/2024 and secured by a first lien on the vehicle. A MAGI phaseout strips the deduction entirely above $150,000 single / $250,000 MFJ. Lenders will issue new Form 1098-VLI beginning in 2026, with transition relief for 2025.

Learning Objectives

After completing this lesson you will be able to:

Background

Personal-use car loan interest has been treated as nondeductible “personal interest” since the Tax Reform Act of 1986. For nearly forty years, the only way to deduct interest on a vehicle was to use the car for business and apportion interest to that business use. The One Big Beautiful Bill Act of 2025 (§70203) carves a temporary exception: a stand-alone above-the-line deduction sitting outside the §163(h) personal-interest disallowance. The provision was promoted as both a middle-class tax cut and an industrial-policy lever to favor U.S. vehicle assembly.

The provision is not permanent — it applies only to tax years beginning after December 31, 2024 and before January 1, 2029. Loans must be incurred after 12/31/2024; pre-existing car loans, even if interest is paid in a covered year, do not qualify.

Rule 1 — The $10,000 Cap and Above-the-Line Treatment

Rule 2 — Qualified Vehicle

| Requirement | Detail |

|---|---|

| New | Original use must begin with the taxpayer. Used vehicles, demonstrators titled to the dealer, and former rental cars do not qualify. |

| Personal use | Cannot be used for commercial, fleet, or rideshare/business purposes. (Use as an employee — e.g., commuting — is permitted.) |

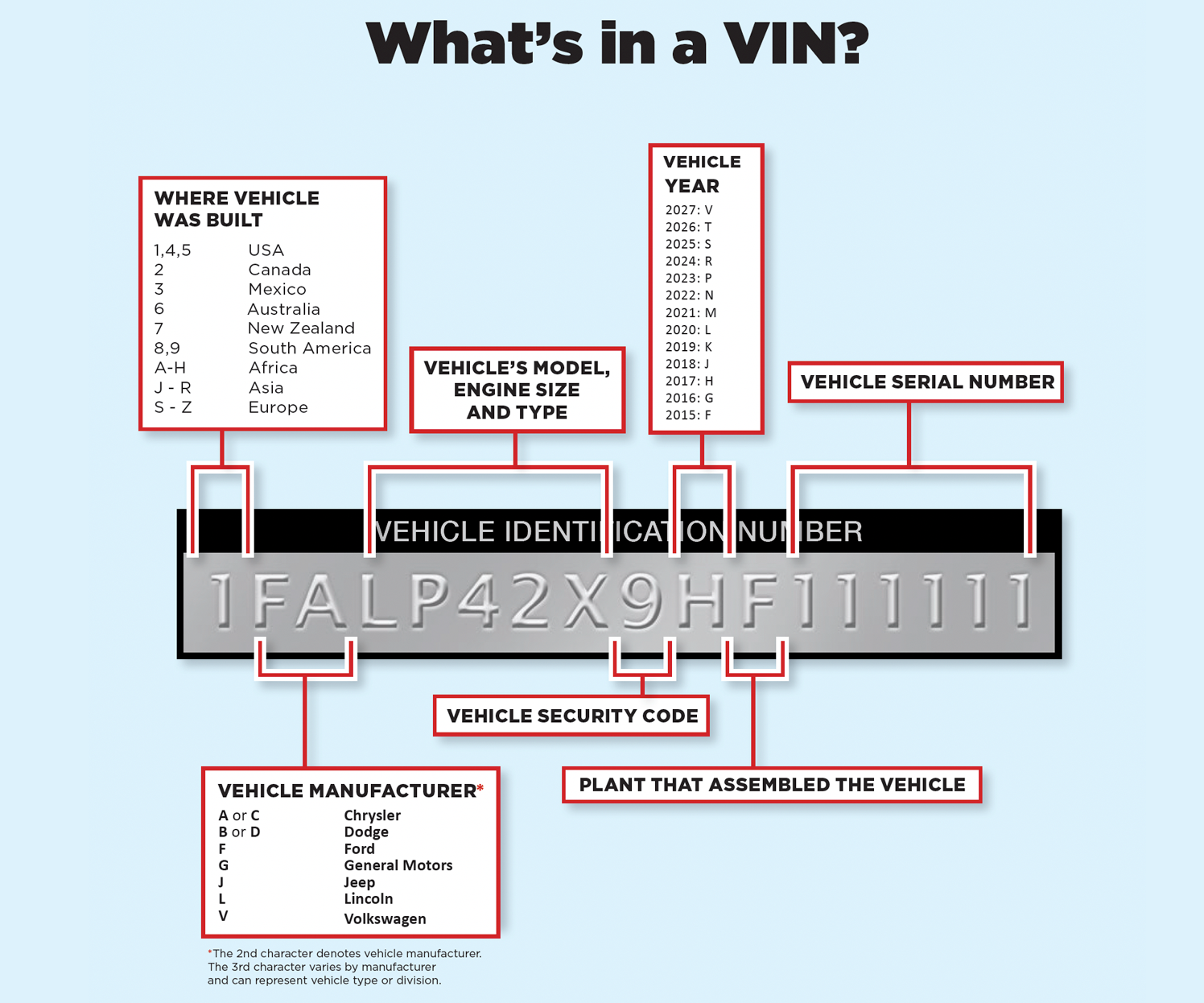

| U.S. final assembly | Final assembly must occur within the United States. Verify against the VIN’s plant code or the manufacturer’s window-sticker disclosure. |

| Vehicle type | Car, minivan, van, SUV, pickup truck, or motorcycle. |

| Weight | Gross vehicle weight rating (GVWR) under 14,000 lbs. Most consumer pickups and SUVs satisfy this; heavy-duty trucks and Class 4+ commercial vehicles do not. |

| VIN reported on return | The taxpayer must include the vehicle identification number on the return claiming the deduction. |

Disqualifying Categories — Spot These Quickly

|

Used vehicles — original use began with someone else. |

|

|

Leased vehicles — leasing isn’t “purchasing”; lease payments aren’t deductible interest. |

|

|

Foreign-assembled vehicles — even otherwise-qualifying brand models may be assembled in Mexico, Canada, Japan, or elsewhere. VIN-check before claiming. |

|

|

Heavy trucks (GVWR ≥ 14,000 lbs) — class-4-and-up trucks are out. |

|

|

Vehicles for fleet, ride share, delivery, or rental business use. |

|

|

RVs, ATVs, golf carts, boats, snowmobiles — not “passenger vehicles” within the §70203 definition. |

Rule 3 — Qualified Loan

Rule 4 — MAGI Phaseout

|

Filing Status |

Phaseout Begins |

Phaseout Complete |

|---|---|---|

|

Single, HOH, MFS, QSS |

$100,000 |

$150,000 |

|

Married Filing Jointly |

$200,000 |

$250,000 |

Example 1 — Standard-Deduction Single Filer, Mid-Range Income

Maria, single, MAGI $75,000. In March 2025 she financed a new Honda Civic (final assembly: Greensburg, Indiana) with a $32,000 loan at 6.9% over 60 months. Her 2025 interest paid: $1,950. She takes the standard deduction.

No phaseout (MAGI below $100,000). Deduction = $1,950 above the line. Tax savings at 12% bracket: $234. Pre-OBBBA, this interest was nondeductible personal interest worth $0.

Example 2 — Foreign-Assembled Vehicle Disqualifies

Same Maria, but she chose a Toyota Corolla assembled in Cambridge, Ontario, Canada. Despite identical loan facts and the new-purchase status, the vehicle fails the U.S. final assembly requirement. Deduction: $0.

Practitioner tip: same nameplate often comes from multiple plants. The window sticker (Monroney label) discloses final assembly, and decoding the first character of the VIN (1, 4, or 5 = U.S.; 2 = Canada; 3 = Mexico; J = Japan; W = Germany; etc.) is a fast first cut.

Example 3 — Phaseout in Action (Single Filer)

James, single, MAGI $128,400. He paid $7,500 of interest in 2026 on a qualifying U.S.-assembled new pickup loan.

Excess MAGI: $128,400 − $100,000 = $28,400. Round up to next $1,000 increment: 29. Cap reduction: 29 × $200 = $5,800. Reduced cap: $10,000 − $5,800 = $4,200. Allowable deduction: min($7,500 interest paid, $4,200 cap) = $4,200.

Example 4 — Phaseout, MFJ, Cap Hit

Aisha and Marcus file jointly with MAGI $215,000. They paid $11,200 of interest in 2026 on two qualifying vehicle loans (a U.S.-assembled SUV and a U.S.-assembled motorcycle).

Excess MAGI: $128,400 − $100,000 = $28,400. Round up to next $1,000 increment: 29. Cap reduction: 29 × $200 = $5,800. Reduced cap: $10,000 − $5,800 = $4,200. Allowable deduction: min($7,500 interest paid, $4,200 cap) = $4,200.

Example 5 — Refinance Preserving Qualified Status

In 2025 the Patel family financed a U.S.-assembled SUV with a $40,000 loan. By July 2026 the principal balance is $34,500 and rates have dropped. They refinance with a different lender for $34,500, secured by first lien on the same SUV.

The refinance qualifies — new loan is secured by first lien and does not exceed the ending balance of the original. Interest paid on the new loan continues to be deductible (within the $10,000 cap and phaseout). If they had instead refinanced for $40,000 to take $5,500 cash out, the post-refinance loan would lose qualified status entirely — even the portion equal to the original balance.

Example 6 — Rideshare Driver, Personal-Use Failure

Ben drives full-time for Uber and Lyft. In 2025 he financed a new U.S.-assembled hybrid sedan with a $32,000 loan, paying $1,800 of interest. Approximately 70% of his vehicle’s miles are for rideshare.

Because the vehicle is used in a business activity (rideshare is self-employment), it fails the personal-use only requirement. Deduction under §70203 = $0. However, Ben can still deduct 70% of the interest as a Schedule C business expense (or use the standard mileage rate, which already includes interest), preserving most of the tax benefit through a different mechanism.

Practitioner Tips

Common Errors / Red Flags

Form 1098-VLI Reporting (2026 onward)

OBBBA §70203 created a new information-reporting requirement: lenders that receive $600 or more of interest on a qualified vehicle loan from an individual must issue Form 1098-VLI, Vehicle Loan Interest Statement, by January 31 of the following year. The form will show: